Do Payday Loans Stop People Getting The Support They Desperately Need?

- New research from Durham University Business School states that the stigma of payday loans causes negative mental wellbeing side effects for loanees

- These loans make borrowers more vulnerable and could be stopping them from getting the support they need

- The researchers call for payday loans to be regulated similar to gambling, smoking and other stigmatised industries

It is estimated there are currently around 14 million people in the UK living in poverty – just over 20% of the population. With a current cost of living crisis affecting not only household bills but the price of food and everyday purchases too, rising rents and mortgages alongside low pay and wage freezes, particularly in the public sector over recent years, it’s likely that the number of people struggling is far greater than that.

Other than tightening your belt, there is often little you can do to make your way out of poverty if it is deeply entrenched. And how can you tighten your belt if it is already tight as it is? The option to shop smarter or make smart investments often isn’t open to those with limited means. With a small amount of cash, you really can only buy cheaper products which might fix a short-term problem but perhaps won’t be effective in the long-term. For example, buying a pair of cheap shoes that you can afford might solve your immediate footwear needs, but it’s likely the quality will be poorer than a more expensive pair, causing them to wear or break sooner and requiring the need to buy yet another pair not too far down the line. Overall it works out cheaper to buy the more expensive, higher quality shoes that will last longer, but what do you do if you cannot pay the initial price? Clearly there is a barrier to entry.

Typically when there is a cost barrier to enter a market or purchase a product, banks can step in to help out – but this comes with interest of course. Think of entering into a mortgage to buy the houses you otherwise couldn’t afford – or securing a bank loan to make big purchases like cars, furniture or electronic goods. Whilst it helps out the consumer in the short-term, the loan is only worth awarding for the bank if there is significant enough level of interest to be gained from it.

Money for Nothing?

Whilst the bank might be more than happy to help you get on the property ladder, its not going to led you the cash to do the weekly shop. Yet, this is something that a lot of people living on a bootstrap budget need – a little help one week that they can pay back the next. And with this gap in the market, where there is demand but no supply, controversial payday loan companies have stepped in, providing financial relief on the small scale to the everyday person.

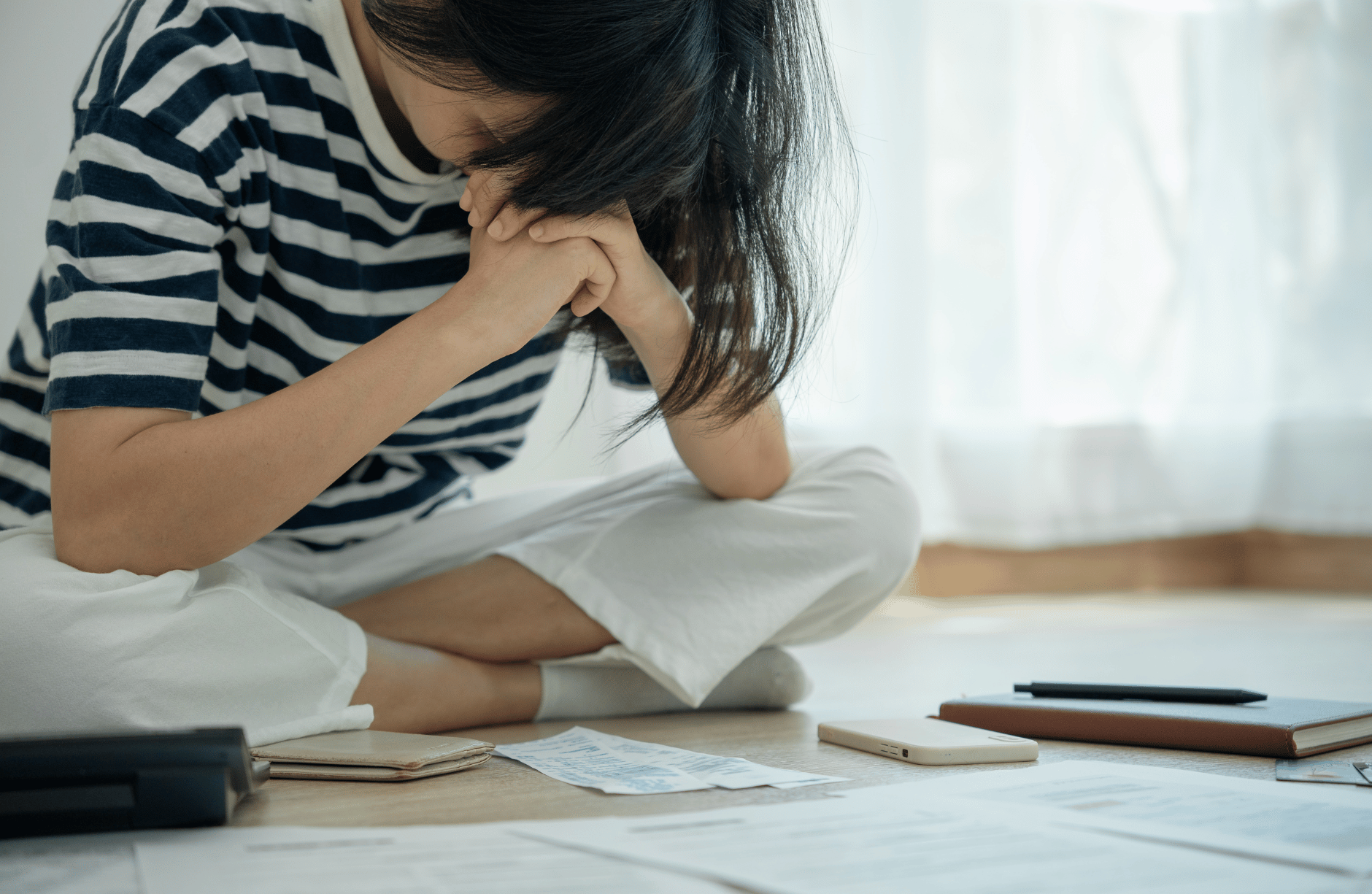

However, such companies are not doing this out of the good of their heart – there is profit to be made when preying on vulnerable people with limited options for help. And the interest rates incurred not just for borrowing but it the event of failing to keep up with repayments can be steep.

Although there is anecdotal evidence that, for some, these payday loans have indeed helped them out of a sticky situation, there are also plenty of stories about how taking out such agreements has plunged people even further into debt and holding them in poverty for longer.

And yet for all the anecdotal evidence and despite the high stakes involved in such schemes, we do not know the wider effect that payday loan companies can have on individuals who use them. Aside of wider financial complications such as growing debts and the subsequent impact to credit ratings, there is also the spillover effects onto the family and friends of borrowers, as well as wider social and financial environment of borrowers too.

This is something that Chrysostomos Apostolidis, Associate Professor of Marketing at Durham University Business School, alongside his colleagues Dr Jane Brown, Newcastle University and Prof Jillian Farquhar, Solent University, wanted to understand. To do so, the researchers interviewed a number of payday borrowers in the north of England, as well as the friends and family of people who had borrowed and people involved in the payday loan industry. The interviews explored their lived experiences with and impact of payday borrowing.

From this, the researchers found three overarching effects that payday loans can have on the borrowers;

A Bigger Cost

Firstly, they discovered that payday loans not only spiralled users into more debt due to the high interest rates they demand, but also the stigma such loans typically have attached to them. This can be incredibly damaging to the users financially – history of payday loan use does not cast the most positive light on an individual’s financial stability after all – but also, as a further consequence, can significantly impact borrowers’ emotional, social and mental wellbeing.

Secondly, payday loans were revealed to affect the relationships borrowers had with their family, friends and other members of society. The research revealed how users often hid the fact that they had or were using such loan schemes due to the stigma surrounding them. Furthermore, concealing their use further compounded the negative effects such loans can have as it limited the opportunity for borrowers to get the support they needed – whether emotional or financial – because of the shame or embarrassment they felt as a result of using the service.

So are payday loans always a bad idea?

Despite the significant downsides the research recorded, there were some positives. The final key finding revealed that some payday loan users had positive experiences with the service, stating that it had enabled them to access the funds required to meet their needs and improve their financial, emotional and social wellbeing. However, the researchers noted that such positive incidences were commonly associated with very careful financial management. The users who found benefit in payday loans were also those who were able to pay the loans back after a short period of time.

With so may people living so close to the poverty line and circumstances unlikely to change, the research highlights a stark need for a more responsible approach to supporting those most in need. “It is estimated that over three-quarters of the UK have some form of personal debt, and unfortunately not everyone can access funds from banks and other traditional lenders,” says Professor Apostolidis. “Many people turn to these short-term, high-interest credit options as a means to plug a gap, however often it is those who are in vulnerable circumstances who fall prey to these loans.”

Without better support, the consequences could be dire. “With the stigma surrounding the use of this borrowing method, many users do not want to admit to using them, which can in turn negatively impact their finances and wellbeing further, causing them to spiral,” he continues.

As problematic as they might be, payday loans do provide many with a vital lifeline. So, what steps can be taken to ensure those who choose to use them do not end up harming themselves or their circumstances further?

This last finding, the researchers say, provides the answer by highlighting the importance of financial literacy and education in reducing debt and financial vulnerability in the society. They call for a greater level of support to be available to payday loan users to help them to meet their repayments, better manage their finances and, ideally, help them to reduce and even eradicate their debts.

To that end, payday loan services should be treated by regulators in the same way as gambling, smoking and other stigmatised industries, due to the impact that their usage has on borrowers’ mental, financial and social wellbeing. Better regulation, they advise, must be put in place.

Interested in this topic? You might also like this…